By Wu Yiyao in Shanghai ( China Daily)

Nonperforming loan ratio rises among top 10 listed lenders

The nation's third-largest lender, Agricultural Bank of China Ltd, will sell nonperforming assetsvalued at 10 billion yuan ($1.6 billion), the bank said on a briefing on Thursday.

ABC is to sell 19 properties used as collateral, along with seven loans, on the Beijing FinancialAssets Exchange, the lender said.

Analysts said that more Chinese lenders may sell nonperforming assets as banks facepressure from souring debts amid an economic slowdown.

|

An Agricultural Bank of China Ltd outlet in Nanjing. ABC had the highest NPL ratio among the nation's17 publicly traded lenders, according to first-half earnings reports on the China Banking RegulatoryCommission's website. Provided to China Daily

|

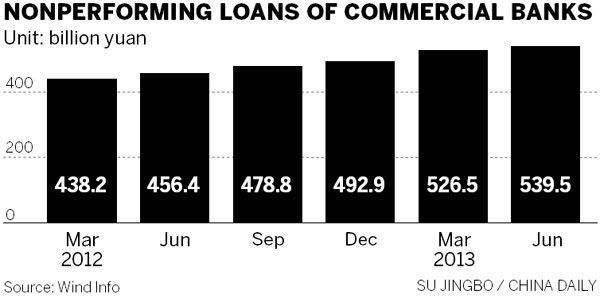

According to statistics from PricewaterhouseCoopers China, outstanding delinquent loans heldby the top 10 listed banks stood at 585.8 billion yuan at the end of June, up 20.42 percent fromthe end of 2012.

The delinquent loan ratio rose from 1.21 percent at the end of 2012 to 1.35 percent at the endof June. The increase signals a possible later rise in NPLs.

The top 10 listed banks are ABC as well as Industrial and Commercial Bank of China,China Construction Bank Corp, Bank of China Ltd, Bank of Communications Co Ltd, ChinaMerchants Bank Co Ltd, Industrial Bank Corp Ltd, China Minsheng Banking Corp Ltd,Shanghai Pudong Development Bank and China Citic Bank International Ltd.

ICBC (the world's most profitable lender), CCB, ABC, BoC and BoComm are the five largestlenders in China. They wrote off 22.1 billion yuan of debt that couldn't be collected as of theend of June, 7.65 billion yuan more than in 2012, according to their exchange filings.

ABC had the highest NPL ratio among the nation's 17 publicly traded lenders, according tofirst-half earnings reports on the China Banking Regulatory Commission's website.

"NPLs are under pressure as economic growth slows, but high levels of loan loss reserves mayprovide a cushion," wrote Christine Kuo, vice-president and senior credit officer of the financialinstitutions group, Asia-Pacific, of Moody's Investors Service in a recent note.

According to lenders' financial statements to the CBRC, as of end-June, the average NPL ratiowas less than 1 percent.

The average loan loss reserve was about triple the level of NPLs.

Writing off the worst of their bad debts will allow lenders to mitigate surging NPL ratios amidrising defaults. Regulators have eased rules for debt write-offs to small businesses since 2010,and policymakers have ordered lenders to improve their risk buffers.

In April, the CBRC urged lenders to increase provisions for defaults, write off some bad loansand curb dividend payments while earnings are ample to create a cushion in case of aneconomic slowdown.

Analysts said that lenders need to improve their risk management skills and pricing capabilitiesunder the increasing pressure of souring debts and contracting profit margins as interest ratesare liberalized.

"The liberalization of interest rates demands a higher level of banks' competence in asset andliability management and interest-rate management. Both the current management models andthe interest-rate gap management tools need to be re-tailored to cope with the dynamicchanges in assets and liabilities, so that banks can effectively manage the interest-rate gapand structural risks," said Jimmy Leung, PwC banking and capital markets leader for China.

"Banks also need to improve their pricing capabilities and optimize their risk managementcompetence, preparing for the final phase of the liberalization in deposit rates," said Leung.