By Alfred Romann in Hong Kong ( China Daily)

Stock markets in China have had a reasonably good performance in recent weeks thanks tosomewhat positive economic data that suggests a change from the slowdown in growth that hascharacterized the economy over the last three-and-a-half years.

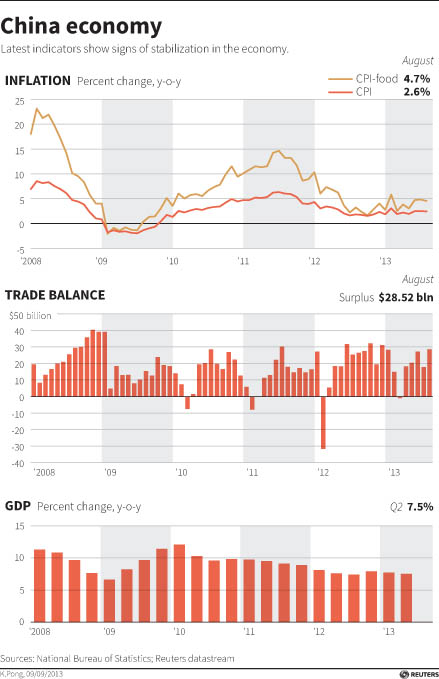

New numbers on industrial production and services suggest China's economy may be enteringa phase of moderate but steady growth after slowing down during 12 of the last 14 quarters.

"There seems to have been a turnaround in economic activity since the financial volatility inJune," says Alaistair Chan, an economist at Moody's Analytics. "The July data were quite strongand we expect that the momentum carried into August."

"The government has been doing some mini-stimulus, but ultimately I think the economy wasnot slowing down as much as it seemed to observers back in June," he adds. "Our forecast isfor growth this year to be close to the government's 7.5 percent target."

China's official Purchasing Managers' Index (PMI) figure, issued by the National Bureau ofStatistics and the China Federation of Logistics and Purchasing, jumped to 51 in August from50.3 in July, well ahead of the 50.6 consensus forecast.

Much of the rise was driven by new export orders, with the sub-index rising to 52.4 in Augustfrom 50.6 in July. New orders also expanded to 50.2, up from 49. The HSBC flash PMI also roseto 50.1 in August from 47.7 in July.

The non-manufacturing PMI dipped slightly to 53.9 from 54.1 in July, but services hit a five-month high in August.

The Markit/HSBC Services PMI, released on Sept 4, came in at 52.8 in August, up from 51.3 inJuly and the highest level since March.

In both cases, figures above 50 signal expansion.

"The rise in new orders set a good foundation for growth in the next few months," said Cai Jin,deputy head of the China Federation of Logistics & Purchasing in a statement.

Many economists were quick to revise their growth forecasts for the second half of the year toas high as 7.7 percent.

The new optimism was widespread but not unanimous.

"It is worth noting that this bounce is occurring within a broad structural downtrend in the surveynumbers," says Rahul Ghosh, head of Asia research at Business Monitor International (BMI).

"Absent a major credit injection and aggressive stimulus plan - both of which appear unlikely -the bounce in manufacturing may prove difficult to sustain," he says.

Still, limited attempts to stimulate the economy are likely to keep growth levels for the rest of theyear, says Ghosh. BMI expects full year growth of 7.5 percent.

Interestingly, the return to stronger growth may be driven by domestic consumption and bylarger enterprises that were in a better position to overcome a liquidity squeeze in June, saidTing Lu, chief China economist at Bank of America Merrill Lynch, in a note.

But good news has been fairly even across the economy. The export outlook may also beimproving as demand from developed economies grows and the government continues withplans to eliminate overcapacity.

"The rise of the official PMI was mainly driven by 'new orders' suggesting the ongoingsequential recovery starts to be driven by external demand even although domestic demand isstill the main driving force," added Lu.

Good news for China can be viewed as good news for much of the region.

The increasingly large economy has an ever-growing impact on the rest of the world andparticularly on those nearby economies with particularly close links. The prospect of a hardlanding in China is enough to scare even the sturdiest of policymakers.

In a recent paper, Moody's Analytics economists painted a scary picture of what a hard landingin China would look like. Although less severe than the 2008 global financial crisis, the impactwould be severe.

An output gap of about 5 percent of GDP in the Chinese mainland would have a severe effecton economies such as Singapore, Taiwan, Hong Kong, Malaysia, Thailand and South Korea.

Singapore, for example, could see output drop by as much as 10 percent of GDP. SouthKorea's output could drop by about 6 percent. The others would be somewhere in the middle.

Less affected would be other countries, such as Japan, India, New Zealand, the Philippines,Indonesia or Australia. Japan could see a gap of 5 percent while Australia would likely lose outon about 1 percent of its GDP.

"China clearly has a big impact but any hard landing there would affect the rest of Asia lessthan the 2008/09 global financial crisis," says Moody's Chan.

Part of the reason for this lower impact is the role China plays in export markets. China is thebiggest export destination for many products but it is not always the final one.

Electronics and components, for example, are exported to China and assembled into fullproducts that are then shipped to sellers in the US, Europe or even back to the countries fromwhich the components originally came.

Continuing demand abroad for products that pass through China would temper a hard landing.

In other words, growth in the US would slow slightly but it would not come close to pushing thecountry into any kind of recession, according to Moody's Analytics.

Countries such as Malaysia and Thailand would suffer more because they rely on China topurchase about 12 percent of their exports. The domino effect would also hit privateconsumption in those countries, not only as a result of lower wages and lost jobs but alsobecause of the negative effect of bad news coming from China.

This is a worst-case scenario that would exacerbate a shift already underway.

"For the most part, the emerging market universe is undergoing a serious re-pricing of risk viahigher borrowing costs, equity market losses and major FX depreciation," says Ghosh.